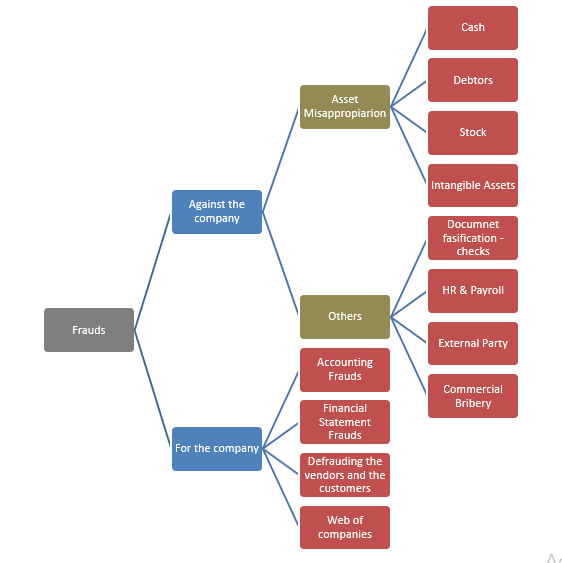

| Type of fraud, Division and Country | What was the fraud and how was it discovered | Action taken by the company |

| Asset – Cash; Courier; India | ESTL used to the do intercity courier services. ESTL had a policy of not rejected business and hence if the customer hasn’t been approved as credit customer, the delivery boys were allowed to collect cash while picking up the consignment. In some case, the deliveries boys picked up the consignments and delivered the same as per ESTL rules but didn’t report sales and pocketed cash. In one particular case, the delivery boy failed to deliver the consignment and called the toll-free number to check about the delivery and that is how fraud was discovered. | When customer wanted the delivery service, the customer is supposed to call toll free number and the call center would call the delivery boy about the prospective customer. The mistake company did was that the call center never called back the prospective customer to check whether the consignment was picked up. The company sacked the delivery boy. |

| Asset – Debtors; Courier; India | When customers paid cash against pending invoices, the delivery boys used the money for good amount of time before was deposited in the company bank account. Since, the company had a policy of checking unpaid dues only at the month end, this practice went unnoticed for quite some time. It was detected only when internal audit division called the customers in the middle of the month and customer told that the money has already been paid. | The company didn’t give receipt book to the delivery boys to give a proper receipt and even the customer didn’t insist on immediate receipt. A classic example where the intention of the customer is not to make a fraud, but his inaction led to a substantial fraud. The company sacked the delivery boy. |

| Asset – Debtors; AV; India | This Salesman had a unique way of protecting his own customers. He used to prepare a delivery challan in the name of Customer A and then deliver the goods to customer B. He used to do this as the credit limit of B would be over and system wouldn’t allow deliveries to B. Later, he would change the invoice and delivery note in the name of B. This way, he used to give more goods to customer B over his credit limit. The company discovered this methodology due to frequent changes in the delivery challans as well as similar delivery addresses. | The company could not prove that the salesman was getting any monetary benefits and hence couldn’t take any action against the salesman. In fact, it took a long time to establish that there was a fraud. The company banned the changes in the invoice and delivery challans without the approval of territory sales manager, but no action was taken against the salesman. |

| Asset –Debtors; Real Estate; India | The salesman used to pre book sales and show commission on the sales as debtors. The said commission would be collected on the completion of transfer of property or registration of rental agreement. This completion may take even up to six months depending on the complexities of the transactions. Out the total commission, part of the amount (even sales) were written off (often collected in cash and never reported to the company) saying that the commission is reduced due to change in the terms and conditions of the sales. This was a continuous trend and ESTL accepted this as a business practice. | The company changed the practice of pre booking sales and started booking sales only on cash basis. This saved the commission on the targets achieved but ESTL was never comfortable if all commissions were brought in the books. This is business hazard and prevention of fraud totally depended on the honesty of the sales staff. |

| Asset –Stock; Trading; UAE | Trading Division in UAE had one of the biggest ship chandlers as their prime customers. Being ship chandler, the orders were never fixed, and goods were always on sale or return basis. ESTL used to procure goods from all over UAE and supply to them. Once the unsold goods are returned, ESTL used to return the goods directly to their vendors. The goods were never returned in full to ultimate vendors and reported to the company as sold to the ship chandlers. There always used to be discrepancies and always took a lot of time to resolve those issues as ships stay used to be brief in UAE. Ship chandler got fed up with these discrepancies and stopped doing business with ESTL. They blamed ESTL’s inability to resolve these issued within reasonable period. | ESTL never took these issues seriously saying that there is no stock holding and are earning good commission by procuring and delivering goods. These goods were never in warded in ESTL’s books and hence receipts and sales were on cash basis. In other words, there was no internal control of any sorts. ESTL started following proper system for recording all transactions. It also showed lack of interest on the part of senior management as they were happy earning howsoever little commission by just delivering the goods and staff took proper advantage of the situation. The staff was dismissed and ESTL after reconciling accounts recovered whatever amount they could by way of selling his assets and end of service benefits. |

| Asset –Intangible Assets; AV; Kenya | ESTL received television sets and a music system for servicing in their Nairobi service center. The customer did not have the guarantee card and requested service at a cost. The company agreed. When the service department opened up the piece, they could neither match the batch number nor the serial number of the piece. Hence they asked the customer for the purchase detail which he did not have and could identify on the store from where he bought the piece. Upon further investigation, it was found out that it was a duplicate piece, and someone was using ESTL brand and selling cheaper articles. | It was clearly a brand abuse and infringement of trademark and patents. The company took the legal action against the store that was selling price. The company also increased brand awareness by advertising in local newspapers about the ownership of brand and possible legal actions. |

| Others –Document falsification Checks; Trading; UAE | The company had a practice of issued printed checks. Unfortunately, one day the machine did not work, and company issued handwritten checks on that particular day. One of the staff members used the opportunity to add few words on the check and encased the cash check with higher amount. It was discovered at the end of the month during bank reconciliation, by that time, staff had resigned and left the company. | The treasury started checking bank statements on a daily basis. ESTL also started the affix see through stickers on the checks making alterations impossible. ESTL also took legal action against the staff though didn’t go through the criminal proceedings due to higher costs involved compared to the existing damage which sent wrong signals to the staff as well as to public at large. |

| Others –HR & Payroll; Trading; Kenya | The company had an obligation to employ minimum number of locals in the company. The fraudulent prevailing practice was to get the documents of few locals and show them as employees. They were paid only 40% of payment in cash against what is shown in the books and to the Govt. The balance money was brought in the books by way of other receipts in two or more installments in order to fend off the taxman. The company was supposed to bring back 60% of the amount by way of other receipts though the amount started reducing month by month. The explanation given by the local management was that tax man have become more inquisitive and need to pay them more on a monthly basis in order to keep this entire transaction under the wraps. In fact, the amount was siphoned by the local management. The issue was discovered as company had no real advantage in continuing this practice. | In this case, corporate management made a grave mistake by letting the local management about the malpractice in which they shouldn’t have participated. The local management took the undue advantage of the situation. The company didn’t take any action against the criminal staff as ESTL felt that removal of local management may lead to closure of African business. |

| Others –External Party; Trading; Sri Lanka | ESTL used to procure tea and cashew from Sri Lanka. There were a lot of malpractices happening in the trade from the suppliers mainly to avoid Government Taxes. As a result, Government had banned many suppliers from entering into trade with the foreign company. ESTL entered into trade agreement with one such party without making any background check on the supplier. Neither supplier give any papers showing his eligibility to enter into trade nor ESTL made any enquiries with Government if the supplier is eligible to trade with foreign companies. ESTL was in rude shock when the export consignment was rejected and fined for trading with banned traders/exporters. | ESTL failed, to make any background check on the supplier. By the time, they realized, their license was suspended six months. ESTL made background checks mandatory with third party documentary proofs for all the parties before entering into contract with them including employment contracts. |

| Others –Commercial Bribery; AV; Russia | ESTL imports goods from all over the world into Russia though branded goods come from EU- Finland. These goods must be transported by road from Kotka to Moscow. Getting import licenses from the Russian Govt. was really difficult and using someone else’s license was a common practice with a caveat that you use transportation, marine insurance and custom clearance service from the same party. ESTL had to pay exorbitant charges for all these services with no guarantee that goods will arrive in time. | ESTL established operations in Russia without procuring all the required licenses and hired even staff who had no knowledge of Russian laws and customs. ESTL had no option but fall prey to all mafia agents in order to survive and had not guarantee that they will be profitable. ESTL did not do proper sovereign risk assessment. ESTL had to wind up Russia operations. |

| For the Company- Accounting frauds | One of the accountants in ESTL acted in collaboration with the customers and created fraud. The sales division was collecting checks from the customers on the due date. This particular accountant would pass appropriate entries and hence customers’ accounts were properly maintained. He then used to call the customers (agree for commission) and used to give them additional credit period by not depositing the checks. As far as collection was concerned, it was on time, but money wasn’t in the bank. This was found out during the monthly Bank Reconciliation Statements. All checks were deposited but none was credited in the banks in time. This also led to late recognition of real dishonored checks which resulted in real losses to the companies. | There is clear lack of internal control over important operations like collections and accounting. ESTL separated the duties and started checking bank credits on the net next day. ESTL changed the duties of the staff and transferred in dispatch division. |

| For the Company- Financial Statement Frauds | ESTL had taken trade finance from the financial institutions. One of terms and conditions was to maintain stocks below particular amount. In reality ESTL had exceeded that stock value. ESTL valued the stock at current market value which was below cost price taking advantage of accounting principles. While doing this, they understated profits and paid less tax to the Government. The fraud was never discovered by financial institutions and ESTL continued to take advantage of accounting rules. ESTL continued selling undervalued stock at higher prices at a later date (presumably when market was favorable) thereby even deferred tax payment to the Government. | Another clear example where ESTL were part and parcel of big fraud and did not set right example for the accounting staff which led to many accounting frauds. |

| For the Company- Defrauding vendors and customers | ESTL used to pay and collect advances for commodities in the international markets. Depending on the price variation ESTL and its suppliers would decide whether to deliver the goods or not. If the contract is entered into a price X and then price has gone X ++, the supplier would enter into contract with another buyer and forfeit the contract with ESTL. ESTL would similar would follow similar practice, if prices fall after entering into contract. Nobody ever considered it as fraud and practice prevails. | ESTL started using this practice as options and futures contract by squaring of advances and started treating this as a profit center. Prima facie, nothing wrong in it, except that at the time of entering into contract other party would not know that they are entering into paper contract. |

| For the Company- Web of companies | ESTL had operations in India, Russia and Kenya and besides India, other two countries have very weak banking system. ESTL had very high proportion of cash transactions in these countries and this cash was utilized by way of financing for purchases in those countries and usually used to find its way into India. In India, ESTL would receive either part or full amount in cash and would be shown as cash sales. Since there was a huge difference in tax rates of different countries, ESTL would use this route to reduce its tax liabilities. | Everybody in the company believed that it’s an effective way of resource utilization and no one ever considered it as a fraud against exchequer. The practice continued and sometimes ESTL paid heavy one-time taxes though this again was considered as cost of doing international business. |